In an ideal world, your 20s are all about having fun. But in reality, most 20-somethings have trouble figuring out their lives, especially in financial terms. The good thing is you have the time. You are right at the cusp of making some of the smartest money moves that will pay off later in life, even into retirement.

Yes, you read that right! Retirement is something you should be planning for today. Before you start thinking of ways to procrastinate retirement planning, read about EPF pension. EPF or Employee Provident Fund is a financial tool that helps you set up a retirement fund early in life. Even if you are working an entry-level job, pension contribution in EPF is a simple way to put together a retirement fund, without giving it much thought.

Let’s understand how EPF pension works!

Key Takeaways

- EPF comprises of three different schemes – EPF, EPS, EDLI.

- EPF pension applies to your basic salary which includes basic pay and Dearness Allowance.

- The interest rate for EPF pension is reviewed every fiscal year.

- EPF investments are classified as Exempt, Exempt, Exempt (EEE) under taxation laws.

What is EPF Pension?

EPF is made up of several different schemes. It consists of three independent plans, each with its own set of goals.

- Your retirement benefits are accumulated in the first portion of EPF. This is the part of the strategy that generates wealth.

- The employee pension scheme is the second component of the EPF (EPS). The goal of EPS is to provide a pension to employees over the age of 58.

- The Employee Deposit Linked Insurance Scheme, or EDLI, is the EPF’s third and final component, which is a life insurance policy.

The good news is that you don’t have to register for each of these perks separately. You are immediately registered for EPS and EDLI when you register for EPF.

Now, let’s focus on what you actually receive as part of EPF pension!

You contribute a portion of your salary to the EPF plan if you work as an employee. Your employer’s contribution is typically matched with this amount. The remaining funds are then deposited with the Employee Provident Fund Organization (EPFO). You will continue to receive a certain rate of interest on this cash deposited with EPFO each year.

Assume you make a pension contribution in EPF of Rs. 5,000 per month. Your company will match it with a monthly payment of Rs. 5,000. After then, the total amount of Rs. 10,000 is deposited with EPFO. On this sum deposited with EPFO, you will receive an annual interest rate of 8.5 percent (current rate of interest in EPF system). This interest rate changes on a yearly basis.

This is how pension contribution in EPF works at its most basic level. Keep in mind that for EPF reasons, salary refers to only two things: your basic pay and your dearness allowance (DA).

What is Pension Contribution in EPF?

Simply put, employee and employer contributions are combined to form an Employee Provident Fund. Both the employee and the employer are required to pay monthly pension contributions in EPF (12% of the fund’s basic and Dearness Allowance). As an employee, you will receive this money when you retire or if you are unable to work either temporarily or permanently owing to a disability.

Is It Too Early to Invest in EPF?

If you’re in your twenties, working a job that allows you to just make your ends meet, you might question if this is the right time to invest in EPF. The answer is yes. Simply because it’s worth it in the long run.

It is always a good idea to start planning your future early for obvious reasons like more time is equal to more money. Especially in an economy that is not inspiring the strongest of hopes.

Who Can Make Pension Contribution in EPF?

EPF pension is available to you if you work with a company that is registered and engages in activities mentioned in Schedule 1 of the EPF Act. Aside from that, the company’s minimum staff strength should be 20 employees for you to be able to make a pension contribution in EPF.

As an employee, you are enrolled in EPF at your employer’s discretion, and the process is completed entirely by your employer. If you are a business owner who wants to enroll your company in this scheme, you must first meet the eligibility conditions and then submit a few documents to complete the procedure.

Did You Know?

In the 1950s and 1960s, the interest rate for EPF was very low, never exceeding 6%. That was in stark contrast to the 1990s, when PF interest rates were as high as 12 percent!

Source: https://www.etmoney.com/blog/how-does-epf-work/

What is EPF Pension Status? How Do I Check It?

There are multiple ways to check the balance of your EPF pension status online.

- Using the EPFO website to check your EPF balance: You can access your PF passbook through the EPFO website. You can also print the information if necessary.

- Visit www.epfindia.gov.in to learn more.

Image Source: https://www.epfindia.gov.in/site_en/index.php

- Select ‘For employees’ from the drop-down menu under ‘Services.’

Image Source: https://www.epfindia.gov.in/site_en/index.php

- Select ‘Member passbook’ from the ‘Services’ menu.

Image Source: https://www.epfindia.gov.in/site_en/index.php

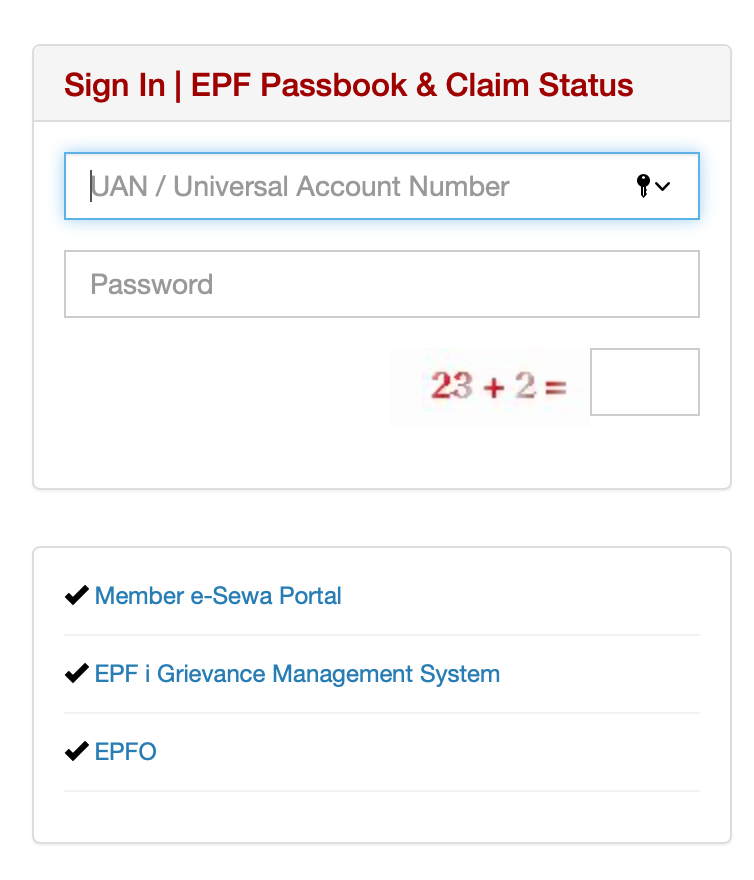

- To view your passbook, enter your UAN and password.

- Although the EPFO offers you with a UAN, you must have it verified and activated by your employer before you may utilise these services.

- Using the Umang app to check your EPF pension status: The Government of India’s Umang app is an excellent tool for checking your EPF balance. You can use this app to examine your passbook, file a claim, and track the status of your claim. You can sign up for the app by entering a one-time password that will be emailed to your phone.

- Sending an SMS to check your EPF pension status: From your registered mobile phone, make a missed call to 011-22901406. Your EPF balance will be sent to you through SMS. This service is also only available if your UAN is linked to your KYC information, i.e., Aadhar, PAN, or bank account information

EPF Pension Rules for Taxation

In terms of taxation, EPF investments are classified as Exempt, Exempt, Exempt (EEE). It has EEE status since contributions are tax deductible. There are no taxes on the money you invest, the interest you earn, or the money you withdraw at the end of the term. This tax benefit, however, is not accessible if you withdraw your investment before the 5-year period has passed.

EPF Withdrawal

There are three instances where you can withdraw from your EPF in its entirety:

- When you reach the age of 58, as a senior citizen.

- If you have been unemployed for more than two months, you may be eligible for unemployment benefits.

- The full corpus is given to the appointed nominee upon the member’s early death.

There are a lot of requirements and conditions to be aware of if you want to withdraw money from your EPF account before retirement. The first of these conditions applies to the circumstances under which you are permitted to withdraw early. And these scenarios include things like education, land buying, marriage, medical emergencies, home loan repayment, and so forth.

EPS Form

When a member changes jobs, they can transfer EPF pension funds to a new account or withdraw funds by presenting an EPS scheme certificate and completing the required EPS form. However, after 180 days of continuous service and before the completion of 10 years, EPS Form 10C can be used to take the accrued pension sum.

Word to Remember

Universal Account Number – Every employee with an EPF account is given a 12-digit number called a Universal Account Number (UAN) by the Employee Provident Fund Organisation. The UAN is transferable and remains constant throughout an employee’s career.

Your 60s Will Thank You for This

Taking charge of your finances when you’re young will make it easier to attain your goals in your 30s and after. It will help you build a solid foundation for your financial future. So, make sure you spend some time thinking about where you want your life to go – and then start moving in that direction.

FAQs

The nominee will receive the settlement of EPF dues with interest, EDLI benefits, and widow pension if the subscriber died while on the job. To receive the EPF pension, the spouse (nominee) must contact the company where their spouse worked.

An employee with a base salary of more than Rs. 15,000 who has never been a member of the EPF can opt out. They cannot, however, opt out of the scheme after they have joined.

In this situation, the accumulated sum shall be transferred to the employee’s fund, or, as the case may be, to the Provident Fund of the institution left by him/her, within such period as the Central Government may specify.

No, an employer’s payment to the Employees’ Pension Fund (EPF) cannot be deducted from employee wages. Any such deduction is a criminal offence, according to Section 14(1A) of the Act and is punishable by imprisonment for a term of up to three years, but not less than one year, and a fine of Rs. 10,000.

Read more about Withdraw Pension Contribution in EPF.