In India, the moment we start earning, we are offered two customary pieces of advice: Seek the blessings of God and open a savings account. Every working professional, salaried or in business, has received these nuggets of wisdom from elders, family members and colleagues. It is always wise to save money for future needs. It is highly recommended that savings are a mandatory component of your finances, so you can secure your future and have a ready fund in emergencies.

There are numerous ways one can save money in India. Savings schemes backed by the union government of India and fixed deposits, popularly called FDs, are the go-to options for parking money from earnings into funds for the future. Public Provident Fund (PPF) is one of India’s most popular savings schemes among the gainfully employed workforce. Investing in PPF comes with several benefits. Not only do you receive a corpus on maturity but you also save tax while you are earning. If you wonder how to invest in Public Provident Fund to build a retirement corpus, we have covered it for you.

Dive Into the Good: PPF Benefits You Need to Know

Before we learn how to invest in PPF and understand what investing in PPF brings, let us go back to the part where we discussed savings. You can keep a proportion of your earnings as collateral against the vagaries of the future in two ways: Savings and Investments. You might ask, how does that matter? It does. Technically, both serve the same purpose and are used interchangeably, but savings represent a risk-free fund. It could be money parked in a bank, a post office or any government-backed scheme. On the other hand, risks are inherent to investments made for accelerated growth in savings.

Investing in PPF falls under the small savings scheme. Like other small savings schemes (such as the National Savings Certificate (NSC), Kisan Vikas Patra and Post Office Savings Scheme) it is a long-term plan that fetches you interest on your money throughout its tenure without any of the risks associated with investments such as real estate and stocks. Getting risk-free returns on a PPF investment plan is not the only good of this scheme. PPF is a goody bag, and here are some of the obvious and not-so-obvious perks of opting for this savings scheme.

- No risks: As elaborated in the preceding section, investing in PPF is risk-free and detached from the volatility in the market that comes bundled with investments in real estate, stocks and mutual funds. The government secures your money and returns it with interest upon maturity.

- Tax savings: You can save on taxes even with a minimum investment in PPF makes it an ideal choice for small savings. The tax benefits to the individual flow from section 80C of the Income Tax Act, 1961. This section provides a deduction in the Income Tax that you are liable to pay on earnings in a financial year. Therefore, tax savings from investing in PPF is the proverbial icing on the cake, particularly for an individual in the fixed-income space.

- Minimal investment: One can keep investing in PPF with a minimum annual contribution of ₹500. For beginners, it just takes ₹100 to open a PPF account. This makes a PPF investment plan inclusive. It allows people from every economic stratum to contribute to a savings scheme and take a step toward securing their future.

- Easy advance and withdrawal: PPF is not just a savings scheme but also ensures you against ups and downs in life. Even when it has not reached its full maturity value at the designated tenure of 15 years, you can take an advance against or withdraw a proportion of the money in the seventh year.

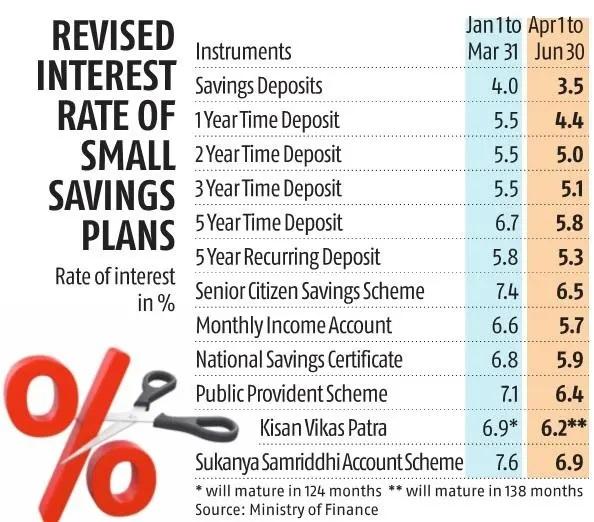

- Better returns than Fixed Deposits: Fixed deposits, which have been a traditionally preferred vehicle of savings, lose their sheen when compared to the year-on-year interest accrued on a PPF investment plan. The interest rate (other than those offered to senior citizens) in most banks varies from a low of 2.5% to a high of 6%. Compared to this, PPF provides an interest of 7.1% that gets compounded every year.

Features of a PPF Account

- Opening balance: You can start investing in PPF by opening an account in your name for ₹100.

- Minimum and max investment: Your annual minimum investment in PPF cannot be lesser than ₹500. The maximum investment in PPF is ₹1.5 lakh in a financial year ending March 31.

- Compounded interest: You are credited an annual interest of 7.1% on your savings in PPF. This interest gets compounded year on year in the books.

- Maturity of PPF: Your investment in PPF matures at the end of 15 years. However, you can choose to extend the tenure of your PPF investment plan a lot of 5 years after its maturity. This facility of extension is without any limit.

- Partial withdrawal: You can make particle withdrawal once your investment in PPF has completed 5 years and is into the 6th year. Partial withdrawal is allowed in exceptional circumstances such as marriage or medical issues.

- Joint account: Investing in PPF is only allowed under an individual’s account. You cannot start a PPF investment plan under a joint account.

- Accounts for minors: PPF account can be opened for a minor. The Guardian, an adult, can continue to deposit money in the account on behalf of the minor until the person is an adult.

- Nomination: Like in most savings and investments, you can designate a nominee for your PPF account.

- Deposit type: There are several options available to anyone investing in PPF for depositing money in the account. You can issue a cheque or deposit cash. You can also invest in PPF online by making a virtual transfer.

- Risk level: A PPF account is a small savings account backed by the government of India, making it a safe investment option. It comes with minimal to no risk.

Did you know?

| Investing in PPF began in 1968 when the National Savings Institute offered the first PPF. PPF savings have now been brought under the Public Provident Funds Scheme Rules 2019, and the older law stands revoked. The interest on a PPF account has continuously dropped over the last 20 years. From a high rate of 12% annual interest in January 2000, the interest rate in 2021 stands revised at 7.1% annually. If, for some reason, the minimum contribution of ₹500 per annum is not made, then your PPF investment plan does not come to a halt. It only becomes dormant. You can reactivate a dormant PPF account for a nominal fee of ₹50 and resume your contributions. Source: https://cleartax.in/s/ppf |

Are You Eligible for PPF Scheme: Find the Eligibility Criteria

If you are wondering about investing in PPF, then you will be relieved to know that it has no major criteria in terms of age or income. Any Indian citizen can open a PPF account and invest in the savings scheme. You can even opt for a PPF investment plan for a minor. In such a case, you can start saving on behalf of the minor as a guardian, and the account gets transferred in the name of the beneficiary upon adulthood. If you are internet savvy, you can simply visit the bank or the post office website and follow the directions on how to invest in PPF online.

Word to Remember: Lock-in period

When you opt for a savings scheme, particularly those that offer tax benefits, you are told about a lock-in period for the money parked in the account. So, what is a lock-in period? The lock-in period refers to a pre-determined tenure for which you have to keep your money with a financial institution. Put simply, a lock-in period bars you from withdrawing money from a savings scheme or an investment such as a Mutual Fund before a cutoff date or maturity date. Investing in PPF also comes with a lock-in period of 15 years, which doubled up as its maturity date. Although, you are allowed partial withdrawals in exceptional circumstances when the PPF investment plan has completed 5 years and is into its 6th year.

There is no best time to invest in PPF but now. PPF combines the best of both worlds of savings and tax benefits. A PPF account is simple to open. Any Indian citizen with ₹100 to spare can enrol for a PPF investment plan with a minimum annual deposit of ₹500. Investing in PPF is risk-free, helps you build a pool of money, and allows you to enjoy a tax deduction every year until its maturity. The best part of opening a PPF account is that it comes in handy in case of emergencies, even before it has reached its maturity. That makes it a perfect savings instrument for the fixed income population looking to save money for retirement. The tax deduction is an added bonus of investing in PPF.

FAQs

No, savings upon maturity and partial withdrawals from PPF are exempted from tax. But you have to declare your income from PPF savings in your tax returns.

PPF account can be only operated under an individual account. You can, however, open a separate PPF account in your wife’s name.

The government of India floats several small savings schemes. These include the National Savings Certificate (NSC), Kisan Vikas Patra, Post Office Savings Scheme, Atal Pension Yojana and Sukanya Samriddhi Yojna for the girl child.

The minimum annual investment to be made while investing in PPF is ₹500.

No. NRIs cannot invest in PPF accounts. However, they are allowed to continue investing in an already existing account.

Read more about PPF Withdrawal Rules.