Post Office Pension Scheme is a scheme where people voluntarily set aside a portion of their savings in pension, which can be withdrawn after retirement. The government introduced this scheme to aid people to have adequate retirement income, and thus, every citizen of India has a secure future.

To promote a saving attitude in people, the government of India established the Pension Fund Regulatory and Development Authority on 10th October 2003 and, in the following year, launched the National Pension System on 1st January 2004.

With better health facilities and sanitary conditions, India will see a rise in the life span, increasing the post-retirement years. According to the United Nations Population Division World, life expectancy is expected to increase from 65 years to 75 years by 2050.

Many do not understand the necessity of pension schemes, but these are one of the ways to maximise wealth and are a safe investment option. With increasing inflation and the standard of living in today’s fast-paced world, it is very important to think of today and prepare ourselves for tomorrow. If you are interested in knowing more about the Post Office Pension Scheme, please keep reading.

Key Takeaways

- Post Office Pension Scheme is an investment option introduced by the Government of India to help all Indian Citizens except NRIs to build a financially stable future after retirement.

- An individual can opt for any post office pension schemes like a Post office savings account, post office recurring deposit, or post office time deposit.

- The highest return is received on the post office monthly pension scheme, thus, making it a very popular choice.

- The Post office pension scheme was launched with a vision to provide financial security to people from each stratum; therefore, another scheme called Swavalamban Yojana was introduced for people who are working in the unorganised sector.

Why should anyone opt for the Post Office Pension Scheme?

The Post Office Pension Scheme provides the subscriber with a unique Permanent Retirement Account Number (PRAN) which remains constant throughout the subscriber’s life and can be used from any location in India.

PRAN allows access to two personal accounts: –

- Tier I Account: This account is for a non-withdrawable sum of money meant for savings. Along with this, subscribers can avail of tax benefits on this account.

- Tier II Account: This Account is a voluntary savings facility. The subscriber can withdraw whenever he wishes but this account does not provide a tax benefit.

The following categories can avail post office Pension Scheme of people:

- Central Government Employees

- State Government Employees

- Corporate

- Individuals

- Unorganised Sector Workers under the Swavalamban Yojana

Benefits of Post Office Pension Scheme

There are several benefits of opting for the Post Office Pension Scheme:

- Transparency– Post Office Pension Scheme is not only transparent but is cost-effective at the same time. The sum of money collected in pension funds is invested in pension fund schemes. The employee can access all the information regarding the investments made and check the value of the investment every day.

- Simple to Use– Subscribers must open an account with their nodal office and get a PRAN. (Permanent Retirement Account Number)

- Regulations– Post Office Pension Scheme is regulated by the PFRDA, Pension Fund Regulatory and Development Authority. The investment norms are transparent and are regularly monitored and reviewed by NPS Trust.

- Tax Benefit– Contribution made in Tier I account allows subscribers to avail of a tax benefit. A deduction of up to Rs. 1 lakh from the total gross income is allowed per section 80C under the Income Tax Act, 1961.

The charges related to Tier I that the employer pays are discussed below:

| Intermediary | Charge head | Service charges* | Method of Deduction |

| CRA | PRA Opening charges | Rs.50 | Through cancelling units at the end of each quarter. |

| Annual PRA Maintenance cost per account | Rs.190 | ||

| Charge per transaction | Rs.4 | ||

| POP (Maximum Permissible charge for each subscriber) | Initial subscriber registration | Rs.100 | To be collected upfront |

| Initial contribution upload | 0.25% of the initial contribution amount from subscriber subject to a minimum of Rs.20 and a maximum of Rs.25,000/- | ||

| Any subsequent transaction involving a contribution upload | 0.25% of the amount subscribed by the NPS subscriber, subject to a minimum of Rs.20/- and a maximum of Rs.25000/-. | ||

| Any other transaction not involving a contribution from subscriber | Rs.20 |

Source: – https://www.india.gov.in/spotlight/national-pension-system-retirement-plan-all

Post Office Monthly Pension Scheme Features

Under the Post Office Pension Scheme, there’s a monthly post office pension scheme. The government also provides these investment options (recognised and validated by the Ministry of Finance) and offers a fixed return on investment.

This scheme provides the highest interest rate of 6.6% compared to other post office schemes like Post office savings accounts, post office recurring deposits, and post office time deposits.

Features of Post Office Monthly Pension Scheme

- Lock-in Period- There is a lock-in for five years. A subscriber cannot withdraw the deposited sum before five years.

- Maximum Limit– The maximum investment made by an individual is Rs. 4.5 Lakh. An individual cannot exceed this threshold even if he applies to multiple post office schemes. The total sum invested in post office schemes should always be up to Rs. 4.5 Lakh. A minor is allowed to invest up to Rs. 3 Lakh only.

- Minimum Limit– A minimum amount of Rs. Any individual can invest 1,500.

- Transferability– A subscriber can easily transfer their Post Office Monthly Pension Scheme account anywhere in India if they are changing their residential status.

- Joint Account– Post Office Monthly Pension Scheme allows a maximum of 3 individuals to open a joint account together. Each investor has an equal right over the account, and the maximum investment threshold is Rs. 9 lakhs, and the individual limit is Rs. 4.5 Lakh.

- Minor Account– An individual can open a minor post office monthly income scheme account in the name of their children. The minimum age limit is ten years, and the sum deposited can be withdrawn after the maturing of the child at the age of 18 years.

- Eligible Residential Status– Every citizen of India is eligible to open a post office monthly income scheme account except non-resident Indian individuals.

Now that we have understood the Post Office Pension Scheme and its benefits. Let’s understand how we calculate the return on investment on the same.

Did You Know?

Individuals above the age of 60 can also open an account under the senior citizen pension scheme post office, and the maximum threshold of the investment amount is Rs. 15 Lakh.

What is a Post Office Pension Scheme Calculator?

As the name suggests, a calculator helps individuals determine how much return they will get if they deposit a certain amount of money in the post office pension scheme.

Let’s take an example and use the post office pension scheme chart to understand this topic better.

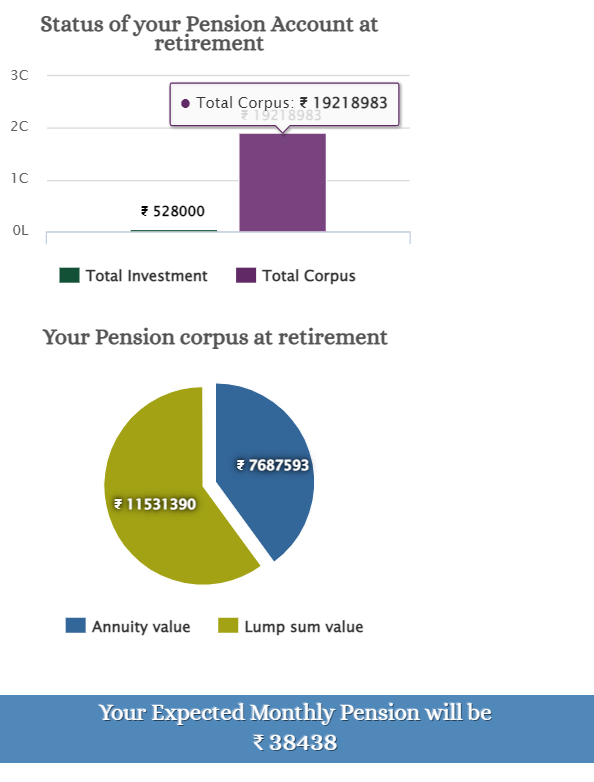

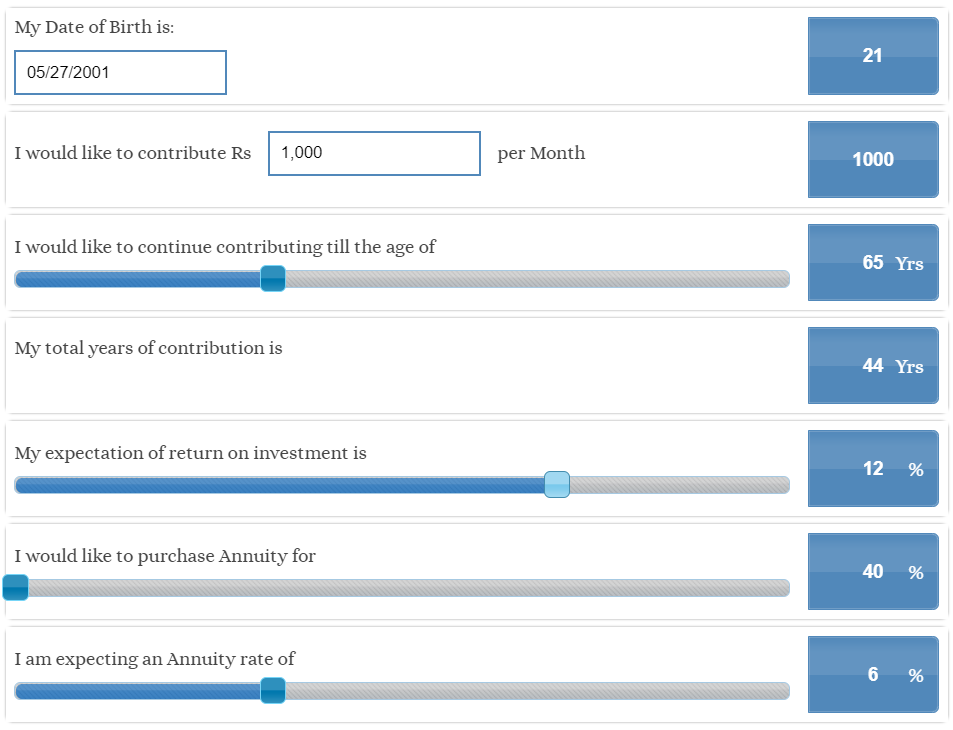

Let’s assume that today is your 21st birthday, and you think of investing Rs. 1000 per month for the next 44 years at an ROI of 12%. With the help of the Post Office Pension Scheme Calculator, we come to the following conclusion:

The total investment made by you is Rs. 528,000.

The total corpus is Rs. 19,218,983; thus, you will be receiving a monthly pension of Rs. 38438.

Word to Remember

Pension Fund Regulatory and Development Authority: It is a regulatory body that keeps a check on the pension schemes offered, and there’s no violation of any rules. It was established on 10th October, 2003, when the government felt a need to help its citizens to develop a saving attitude. The following year the government also launched the National Pension System on 1st January 2004 to motivate people to invest in such schemes and secure their futures.

Last Words

Change is the only constant in life; therefore, to be ready for all types of situations, people need to think about ways of securing their futures. Many people like to invest in the share market, but a person with no knowledge of the markets is simply gambling.

Seeing all these gaps in investment options, the government introduced such post office pension schemes to help people secure their futures financially. The fact that these schemes are backed and validated by the government makes them one of the safest investment options in today’s time.

Therefore, people who do not have sufficient knowledge about ways of securing their future financially can simply opt for this option. This initiative taken by the government will help people across all strata to avail a better standard of life after retirement. By introducing the Swavalamban Scheme, the government has tried to help the people working in the unorganised sector and provide an equal opportunity to every citizen of India to avail of this scheme. Minors can also opt for this scheme, the condition being that they should be above the age of 10 and maintain a maximum deposit limit of 3 Lakhs.

FAQs

Yes, a minor above the age of 10 can opt for this scheme. The maximum investment threshold for such an individual is Rs. 3 lacs, and they can choose to withdraw the entire amount after reaching the age of 18.

Any person above the age of 60 can opt for the senior citizen pension scheme post office by depositing a minimum amount of Rs. 1000 and a maximum amount of Rs. 15 Lakh.

All the citizens of India can avail of this scheme except NRIs. Some examples would include

Central Government Employees

State Government Employees

Corporates

Individuals

Unorganised Sector Workers

Yes, you can refer to the post office pension scheme calculator to know the return value. You can also use a post office pension scheme chart to compare different options you consider investing in.

The following regulatory bodies are present in India-

Pension Fund Regulatory and Development Authority (PFRDA)

Point of Presence (POP)

Central Recordkeeping Agency (CRA)

Annuity Service Providers (ASPs)

Also read about PPO on Investment Simplified.