Retirement is the only time when we don’t have to “hustle”. When we can relax on the beach, sipping our mimosas at the golden hour or travel to different places without a worry in the world, or so they say. But how are we to accomplish this retirement bucket list when we have not saved enough funds? The only way to not risk losing our leisure years is by having sufficient funds that can last for years after retirement.

For someone in their 20s or 30s, planning for retirement is one of the last things to consider. And even before this subject hits our priority list, it is already too late. But to lead a financially independent life after clocking out of our jobs for good, we must start retirement planning as early as possible in our life. However, it is easier said than done with so many options (and opinions) available in the market.

Well, the best place to start is getting our fundamentals sorted. Let us look in-depth at the pros and cons of a retirement plan and the different types of pensions available.

Let Us Brush Up Our Basics:

Did you know that in an India Retirement Index Study conducted by Max Life Insurance covering 1,816 respondents, four out of five people above the age of 50 years feel that they should have begun their planning earlier? So, let us first tackle the question of when to start: The best thing about planning for retirement is that we can begin at any time. But the sooner, the better. This ensures a substantial saving pool to fund our stable (yet happening) retired life.

Some of the other pointers to remember are the following:

- We can choose to acquire our retirement fund in mainly two ways: lump-sum or regular income.

- Annuity types of pensions are known to offer guaranteed income. These types of pension funds work as insurance schemes for long-term savings.

- Importance of equipping ourselves with good health insurance as it can come in handy to mitigate any medical expenses after retiring.

- Frequently check the value of current savings with the calculated retirement expenses.

- Finally, to gain substantially accumulated wealth for tomorrow, cut down today’s unnecessary expenses.

Key Takeaways:

- Starting to plan retirement as early in life as possible leads to a substantial corpus.

- Preparing the required retirement amount depends on several factors that need to be considered and calculated carefully.

- We need to frequently check the calculated retirement amount with our current savings to avoid any inconvenience.

- With so many types of pensions available, choosing the best one depends on our needs and the pension structure.

How do Retirement Schemes Work?

Retirement schemes aid in turning a part of our savings into long-term future income. To do so, a specific amount needs to be invested regularly during the tenure of employment.

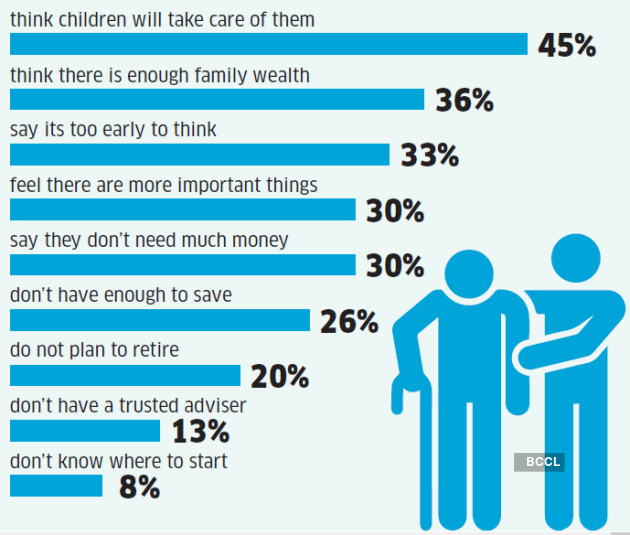

We are offered many types of pensions to invest in, yet did you know that only 1 in every three people saves for retirement?

Reasons people do not invest in retirement planning.

What are Our Options – Types of Pension Plans

Choosing from the types of retirement plans available as the suitable ones for us is quite a difficult task. Several factors need to be considered while opting to invest in a pension scheme but to do so; we will first need to learn about the different types of pension funds.

Each of these types of pensions can be classified specifically according to its benefits and structures. Here are some of the most popular types of retirement plans that we can consider to get started:

- Deferred Annuity Types of Pension Plans – These retirement plans require us to create a corpus that will later be used to purchase an annuity during retirement. We are given the option to buy this annuity in a single-payment mode or a regular premium mode of payment. On the plan’s maturity, a pension will be received. Only one-third of the corpus is tax-free, while the rest is taxable on withdrawal.

- Immediate Annuity Types of Pensions – In this scheme, we deposit a lump-sum amount to receive immediate annuities. We are free to choose the investment amount and the wide range of annuity options. The nominee selected by us will be entitled to these benefits in case of an unfortunate incident.

- NPS (National Pension Scheme) – This scheme is among the two types of pensions offered by the government of India, and we can invest in debt and equity funds depending on our risk profile. We can withdraw up to 60% retirement corpus on retiring, and the rest needs to be purchased for annuity.

- Pension with Life Cover – Most of the types of retirement plans available provide a life cover having annuity options. In case of our demise, the beneficiary will be offered the benefits. Furthermore, the life cover ensures our partner’s financial safety.

- Employee Provident Fund (EPF) – Regulated by EPFO (Employees’ Provident Fund Organisation), this is among the two types of pensions provided by the Indian government. This is a scheme for HUF (Hindu Undivided Family) investors and salaried individuals. In EPF, a certain percentage of our basic wage needs (currently 10-12%) to be contributed which is matched by the employer. Upon our vesting age, we will receive the entirely contributed fund and the interest rate.

Word to Remember:

Annuity – A pension received as regular income after retiring is known as an annuity. We can choose the annuity frequency at our convenience.

Vesting Age – The age we start receiving our monthly pensions. Most types of pensions have a minimum vesting age of 45/50 years and are flexible up to 70 years. However, depending on the insurance company, we can set the vesting age as high as 90 years.

Is There a Need to Plan Our Finances for Retirement?

Did you know that many consider 65 years the ideal age to retire? Even so, covering expenses while having a job is convenient, but what about after retiring? By investing in one of the types of retirement plans, we can ensure the following:

- Cover everyday living costs

- Cover medical bills

- Help fight inflation

- Tackle life’s uncertainties

- Meet retirement objectives

The Bottom Line:

Thriving in the generation that believes in FOMO, it can be quite dreadful and painstakingly realistic to face the fact that in a blink of an eye, we are all going to be senior citizens one day. But that won’t stop us from living our dream and being financially independent. And the only way to ensure that is by planning your retirement ahead of time, if possible, right now. Since several types of pensions are available in the Indian market, we must thoroughly go through each one and choose the one that suits our needs the most

FAQs

Under Deferred Annuity plans, three more types of pensions can be drawn – Indexed, Variable, and Fixed. Fixed Annuities are pensions that offer us a guaranteed or fixed return rate. In an Indexed Annuity plan, we’re liable to the rate of return depending on the market index. However, a variable type of annuity plan is entirely based on the portfolio of the accounts chosen by us (such as Mutual Funds performance).

As per Section 80C Income Tax Act, 1961, all retirement plans are covered and thus eligible for tax deductions of up to Rs. 1.5 Lakhs. However, only the pension maturity amount is tax-free, and the rest of the annuity is taxable.

While ensuring safety nets like PF accounts are essential, they might not be sufficient. To understand how much we can expect out of a pension scheme, we can use a retirement plan calculator depending on the types of pensions available.

Several factors such as desired living standard, requirements of the financial dependents, age of retirement, the value of other assets, and so on must be considered to calculate how much we need to invest in a pension scheme.

Why do we need to start retirement planning early?

We’re constantly told to start investing early because our age can play a crucial role in considerably increasing our retirement wealth. For instance, we aim for a retirement corpus of about Rs. 2 Crores. If we start to invest Rs. 3,500/month in several investment instruments that offer us 12% annually, then our accumulated wealth would depend on the age we begin to invest in the following way:

| Starting Age | Investment Amount | Accumulated Wealth at the Age of 60 |

| 25 years | Rs. 3,500 | Rs. 2.3 Crores |

| 30 years | Rs. 3,500 | Rs. 1.2 Crores |

By starting only five years later, we will lose almost half of the estimated value.

Also read about Widow Pension Scheme on Investment Simplified.