Tax Deducted at Source (TDS) is a popular tax component of an individual’s income. In general terms, TDS is a tax deducted right from a person’s income source.

TDS is based on the concept that every individual who makes a specific payment to another individual is liable to deduct tax as per the TDS rates issued in the Income-tax Act, 1961 immediately at the source and is required to deposit the amount into the government’s account, which the Government will use to improve infrastructure, build healthcare centers for the public and develop rural areas.

If you are a salaried professional, you may have observed a certain amount of deduction from your monthly pay. That amount of tax is nothing but the TDS, which the employer collects to deposit with the government. So now you know why there is a tax deducted from your salary, loans, etc. As a taxpayer, it is crucial to observe and have a clear understanding and knowledge of how this works.

Tax Deducted at Source (TDS), and Tax Collected at Source (TCS) are both taxes charged on the source of income. TDS is the company’s tax deducted from an individual’s salary to pay the government, whereas TCS is the tax collected by sellers while selling to buyers.

TDS interest rate varies from one source of income to another. As we know what TDS means, let’s see why TDS is deducted, how TDS interest rate is calculated, and the different taxes deducted on different sources of income.

Key takeaways:

• In what different scenarios are we liable to pay TDS, and who is not?

• The different types of TDS paid on various sources of income.

• How is TDS calculated on various sources of income?

• How can an individual be eligible not to pay TDS?

• How can a TDS return be filed?

When is the TDS deducted, and who is liable for deducting the same?

- According to Income Tax Act, 1961, any payments paid under this Act are liable to a Tax deduction during its payments.

- If an individual pays a rent of Rs 50,000/- or more, then a TDS interest rate of 5% would be deducted. He need not apply for a Tax Deduction Account Number (TAN) if he is liable for a TDS interest rate of 5%.

- If you are an employee in a company, then your company’s employer deducts a tax based on applicable tax slab rates. The bank which holds your working account will levy a TDS interest rate of 10%. However, if they do not have your PAN details, then the TDS interest rate will be 20% used for deduction. Hence, it is crucial to check for the PAN and ensure it is provided.

- No TDS will be deducted if you submit all required investment proofs and it is below the taxable limit.

- Being a regular taxpayer, one must know that there is a way to avoid paying the TDS.

- If an individual has made certain investments, the same proof can be submitted in Form 15G/15H.

- Once the employer verifies the same, and ascertains that the investment proof meets the criteria, then no TDS is deducted by the employer.

- In case you failed to submit the investment proof to your employer and the bank deducted the TDS, you can file a return and claim a refund provided your total taxable income is below the total taxable limit.

Let us take an example of TDS, assuming the nature of payment is professional fees on which the specified rate is 10%. A company XYZ makes a payment of Rs 50,000/- towards professional fees to company ABC, then XYZ shall deduct a tax of Rs 5,000/- and make a net payment of Rs 45,000/- (50,000/- deducted by Rs 5,000/-) to ABC. The amount of 5,000/- deducted by XYZ will be directly deposited by XYZ to the government’s credit.

Different types of TDS Interest rates

1. TDS interest rate on Salary:

The TDS interest rate on salary depends on the employer’s salary income, and accordingly, an individual will fall into the category of various tax slabs. As per the various TDS interest slab rates, the range of TDS deduction can range anywhere between 10% to 30%.

| Income | Tax Rate |

| Upto `2,50,000 | Nil |

| `2,50,001 to `5,00,000 | 5% |

| `5,00,001 to `10,00,000 | `12,500 + 20% of Income exceeding `500,000. |

| Above `10,00,000 | `1,12,500 + 30% of Income exceeding of `10,00,000. |

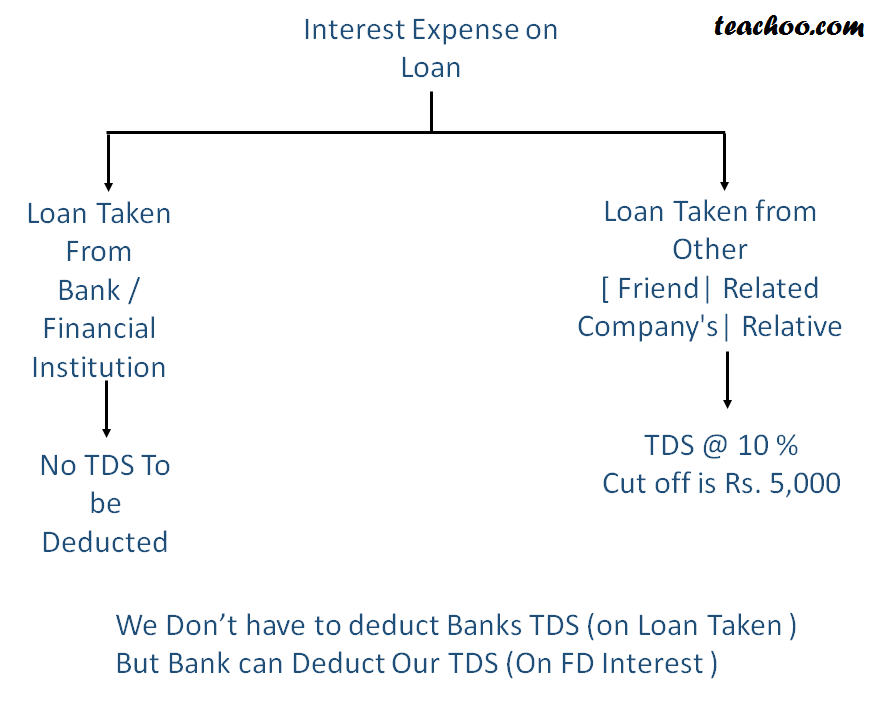

2. TDS on Interest on Loan:

As per section 194A, the TDS on Interest on Loan is deducted at a TDS interest rate of 10%. However, no TDS would be deducted if your interest per annum is less than 5000. TDS is payable only if the interest per annum exceeds 5000/-.

TDS rate on Interest on Loan:

The TDS paid on interest on the loan was 10%, but due to lockdown, it was reduced by 25% (i.e., 10%*75%=7.5%). However, this rate was applicable only from 14th May 2020 to 31st March 2021.

3. TDS on Interest:

Section 194A of Income-tax contains information regarding TDS which is levied on interest such as Interest on Loan, Interest on FD, etc. Interests in securities are mentioned in section 193.

Interest paid to a resident person can deduct a TDS under section 194A, and if this payment is made to a non-resident, then the tax is deducted under section 195.

| Payment By | Rate of TDS | Threshold Limit |

| Other than banks | 10% (If PAN is furnished) | Rs 5,000 |

| Other than banks | 20% (If PAN is not furnished) | Rs 5,000 |

| Banks | 10% (If PAN is furnished) | Rs 10,000 |

| Banks | 20% (If PAN is not furnished) | Rs 10,000 |

4. TDS on Savings bank Interest:

The below table represents the TDS on savings bank interest-

The below table gives a fair idea about the TDS rates for various natures of payment. With the help of the below table, you can identify which TDS can apply to you or your business.

Some of the other TDS rates are:

| Section | Particulars of Payment | TDS Interest Rate for Indian Resident – (in %) | TDS Interest Rate for Non-Resident Indian – (in %) |

|---|---|---|---|

| 192 | TDS interest rate on Salary payment | As per the income tax category | As per the income tax category |

| 194B | TDS interest rate on Income earned through the winnings from lotteries and card games, | 30 | 30 |

| 194BB | TDS interest rate on Income through winnings from horse racing | 30 | 30 |

| 194EE | TDS interest rate on payment made to National Savings Scheme (NSS) deposits | 10 | 10 |

| 194F | TDS interest rate on payment made for repurchase of units by Mutual Funds or Unit Trust of India | 20 | 20 |

| 194G | TDS interest rate on Income made from the sale of lottery ticket | 5 | 5 |

| 194LBB | TDS interest rate on Investment fund which generates to income to the unit holder [other than incomes exempted u/s 10 (23FBB)] | 10 | 30 |

| 194LBC | TDS interest rate on Income generated from investments in securitisation trust | 25 (30% for any other person) | 30 |

Word to Remember:

Liability: The responsibility of a person, business, or organisation to pay or give up something of value.

Interest: Money that is charged by a bank or other financial organisation for borrowing money. It is nothing but a financial cost to the lending authority.

Conclusion:

Now we know where that small amount that is always being reduced from monthly salaries, loans, and your bank accounts is being used for and how it is calculated.

Tax Deducted at Source is a tax paid at the source for different sources of income used by the Government for various features like architecture, welfare, and other things. So this is how a small amount from an individual makes a difference. When the same is viewed from a bird’s eye view, it results in a bigger impact on the overall economy.

FAQs

Answer: A person liable for audit u/s 44AB of Income-tax Act,1961 is liable to deduct TDS as per the relevant provisions.

Answer: The Government uses the money received to improve infrastructure, provide healthcare for the public and improve rural areas. To allow the Government to establish profitable schemes and infrastructure, every individual and company should pay their taxes.

Answer: The Income Tax Act, 1961, is an act passed by the Government to govern all the taxation in the country. It tells us about levying, administrating and collecting taxes for the Indian Government.

The Income Tax act consists of 23 chapters and 298 sections.

Answer: One way to declare it in your IT return form, by which the income tax department will compute and refund the amount back to your bank account.

The other way is to fill out a 15-G form and submit it to your bank, telling you that your income is less than the taxable rate and the TDS cannot be levied on it.

Answer: PAN stands for Permanent Account Number, and TAN stands for Tax deduction Account Number. TAN is for the person responsible for deducting tax, i.e. the deductor.PAN cannot be used as a TAN. Hence, a deductor must perform his work on TDS and deducting and collecting taxes.

However, PAN can be used in some cases instead of TAN when the deductor purchases a piece of land or property.