When deciding on a life insurance plan, the premium you’re going to pay for it and the frequency of it plays a significant role since it’s a recurring job that you’ll be doing for a long period. There are two types of terms in a life insurance, especially in a term insurance: policy term and premium payment term.

What is a policy term and premium payment term?

A policy term is the duration for which the policyholder is getting life coverage. This is significant in the case of a term insurance. Whereas, the premium payment term is the duration for which the policyholder is going to pay the premium for.

Policy term and premium payment term can be the same or different, depending on the premium payment frequency.

What is a Premium Payment Frequency?

Premium payment frequency is the way in which the premium is being paid. There are two variants of it, viz. regular premium payment and limited premium payment. Again, when we are talking about the premium payment frequency, there is further sub-division to it in the form of monthly payment, half-yearly payment and annual payment.

That said, there is another option offered by the insurance providers to some of the customers, i.e. Single Pay Premium Payment Option. With this option, you are required to pay all the premiums in one go, i.e. as a lump sum amount. It is suitable only for those who already have enough surplus and they do not need to worry about removing a big chunk of money from their basket.

What is the difference between limited pay and regular pay in term insurance?

As mentioned before, limited pay and regular pay are the two types of premium payment options that the policyholder can choose at the time of buying a term life insurance. But what’s the difference between the two? In the former option, premium is paid for the entire duration of the policy term, i.e. if the policy term is 40 years, then the policyholder is going to pay a premium for the same – 40 years. Whereas, in the latter option of limited payment, the policyholder is given the option to pay the premium for a short duration of time. Such a duration is less than the policy term.

Also, the premium amount in the limited payment option is more than that of a regular payment option simply because the duration of paying premium is less. That said, life coverage as well as the policy term remains intact after the premium payment term is over.

The following table further makes the distinction between the two quite clear:

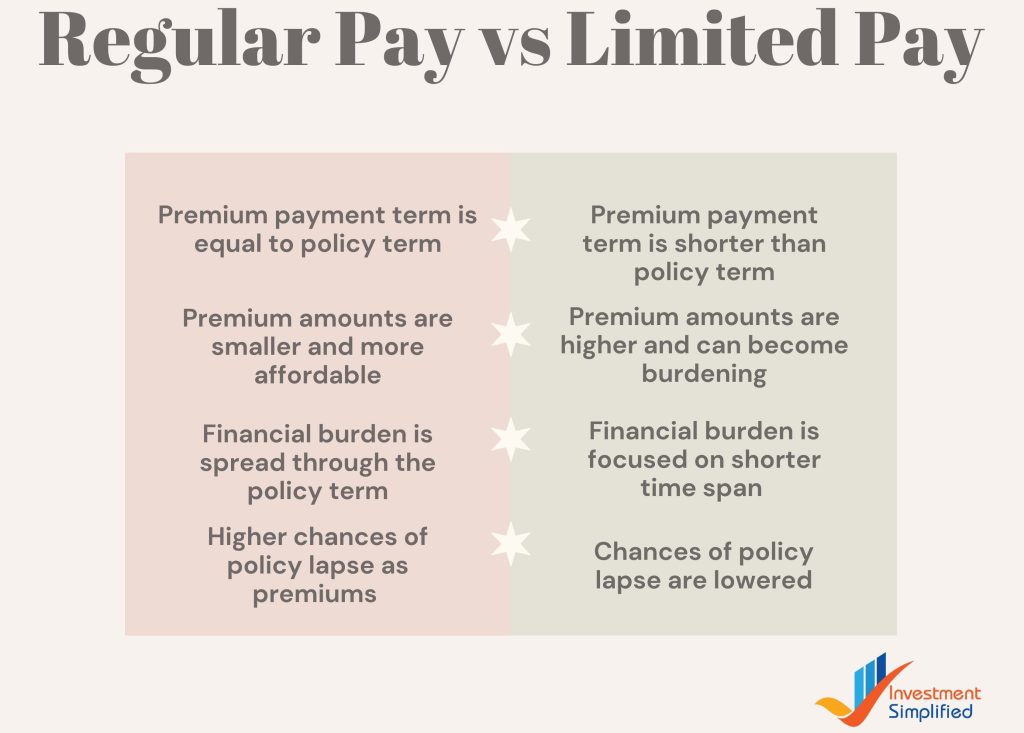

| Regular Pay | Limited Pay |

| Premium payment term is equal to policy term. | Premium payment term is shorter than policy term. |

| Premium amounts are smaller and more affordable. | Premium amounts are higher and can become burdening, in case of a financial imbalance. |

| Financial burden is spread through the policy term. | Financial burden is focused on a specific and shorter time-span. |

| Here, liability of premium payment is stretched till the end of the policy term. | This option allows for quick riddance of premium payment liabilities. |

| Higher chances of policy lapse as premiums are to paid for a long period of time. | Chances of policy lapse are lowered since the premiums are to be paid for a shorter period. |

Which is Cheaper: Limited Pay or Regular Pay Option?

To put it straight, when you choose the limited premium payment option, you pay less premium as compared to the regular premium payment option. This difference amounts to about 40-50%. Let’s understand this with the help of the following example:

X, 26 year old male, wants to buy a term plan till his age of 60 years (i.e. 34 years of coverage) for a sum assured of Rs 1 crore. He choses Max Life Insurance Smart Secure Plus plan for this. The following are the findings:

| Particulars | Monthly Premium | Total Premium |

| Pay till maturity (34 years) | Rs 795 | Rs 3,24,360 |

| Pay till age 41 (15 years) | Rs 1,127 | Rs 2,02,860 |

| Pay till age 36 (10 years) | Rs 1,505 | Rs 1,80,600 |

Conclusion:

- Difference between paid till maturity & paid for 10 years = Rs 1,43,360 (44% savings)

- Difference between paid till maturity & paid for 15 years = Rs 1,21,500 (37% savings)

Which is better for me: Limited Pay or Regular Pay?

Now that we’ve understood the basic idea behind a limited premium payment option and a regular one, how do we decide which one to choose when buying term life insurance? The following factors can help you make an informed decision:

What is your nature of job?

If you have a stable source of income then you can go for the regular pay option, otherwise if your income is not stable, i.e. if you’re a business-person or a freelancer, etc. then going for the limited pay option might suit you better.

What are your retirement plans?

Will you have a source of income post-retirement? If you are affirmative, hit the regular payment option as you’ll be able to pay your premiums easily even when your salaried job comes to a halt. If not, limited pay is the better fit.

What is your nature of work?

Some of us have a desk-job while the others might be involved in a field-job or something like that of a pilot or civil engineer in mines and such places. For those in the latter type of jobs, limited premium payment option is good as their life is more unpredictable.

Some of the top term plan providers offering limited pay and regular pay options:

| Insurance Provider | Premium Payment Option | Special Features | Claims Paid Ratio (FY 22-23) | Assets Managed (FY 22-23) |

| Max Life Insurance: Smart Secure Plus Term Plan | Regular, Limited and Single Pay | 64+ critical illness covered with rider, 5% premium discount on buying online, terminal illness cover at 0 additional cost, premium break (can skip premium after 10 policy years) | 99.51% | Rs 1,22,856 Crores |

| Tata AIA | Regular, Limited and Single Pay | Option to increase life cover at a later stage, preferential rate for women, quick claim settlement, etc. | 98.53% | Rs 24,025 Crores |

| Bajaj Allianz | Regular, Limited and Single Pay | 1% discount on online purchase, 5% off on first time life insurance buyers, etc. | 99.04% | Rs 73,773 Crores |

| ICICI Prudential | Regular, Limited and Single Pay | 34 critical illness with rider, life coverage up to 85 years, etc. | 97.80% | Rs 2511.91 Billion |

In conclusion, we would like to reiterate that it is important to thoroughly analyze your source and stability of income, the nature of your job and your future plans when finalizing the premium payment mode for your term insurance plan. Please note that you will not be able to change your premium payment mode once the policy is sold to you. Thus, do your research and choose a plan that suits your needs the best and also fits your budget.

Limited Pay vs. Regular Pay for Term Plan: FAQs

A limited pay option is where the policyholder will pay the premiums of their insurance policy for a limited period of time only, instead of paying throughout the policy duration.

Regular pay option is where you pay your insurance premiums regularly, i.e. throughout the policy duration.

Premium break is a year in which you do not have to pay the premium and the polic will not lapse. There are some companies that offer this facility of premium break, viz. Max Life Insurance (twice in the premium payment term period), India First Life, etc.